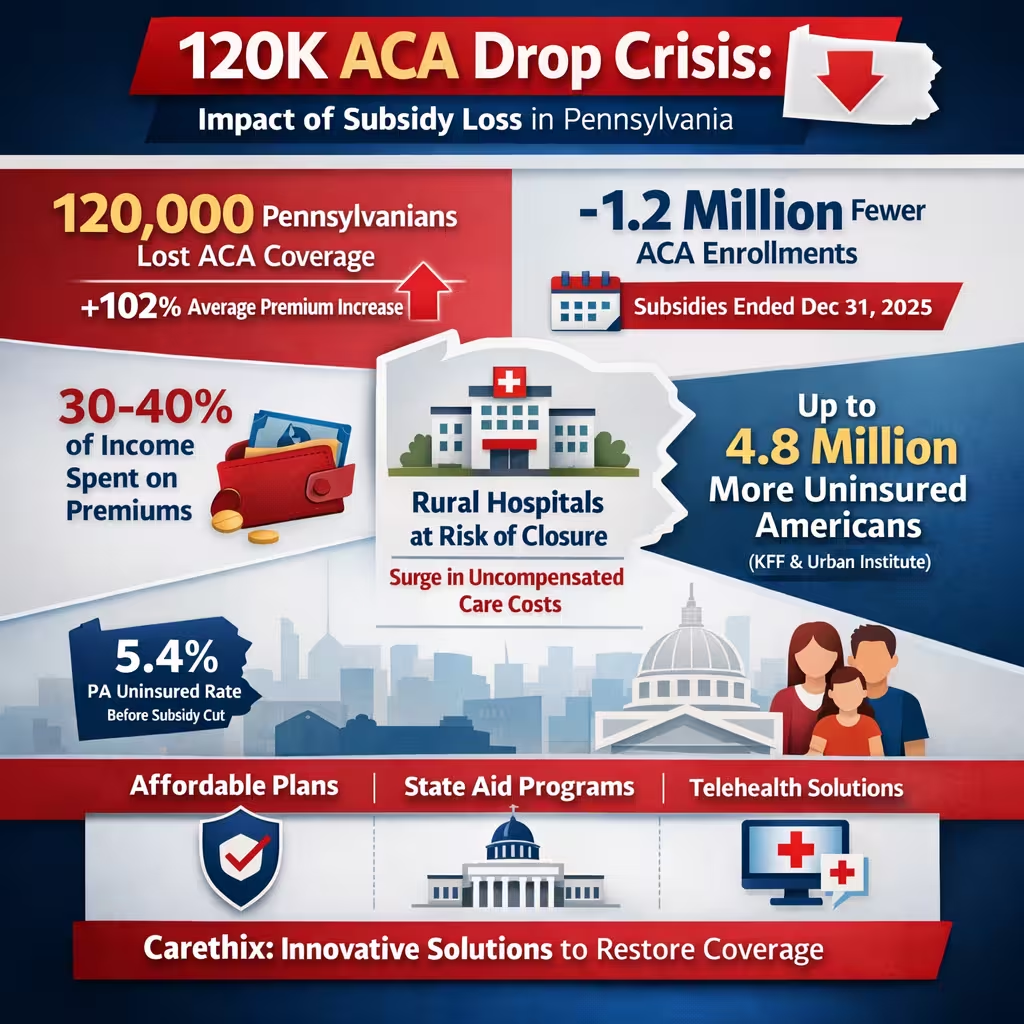

120,000 Pennsylvanians have dropped ACA health insurance since the loss of federal subsidies, forcing tough choices between premiums and basic living costs like rent and groceries. The significant 102% surge in average premiums, without the buffer of enhanced tax credits, has created a severe crisis, dramatically increasing the risk of medical debt and deferred necessary care for many families. At Carethix, we are committed to forging intelligent coverage solutions. Our strategies are designed to stabilize the financial situation for both individuals and healthcare providers, ensuring essential access to care is restored.

Pennie data shows enrollment fell from 497,000 to 486,000 by early 2026, with about 1,000 people dropping coverage daily during open enrollment. Nationally, ACA plan selections dropped by 1.2 million compared to 2025 levels, signaling broader fallout from the subsidy expiration that ended December 31, 2025. These numbers reveal how high costs compound with inflation, pushing even moderate-income households over the edge.

The pain point runs deep for working families who once relied on subsidies to cap premiums at 8.5% of income. Without them, many now face full sticker prices that consume 30 to 40% of monthly budgets. Carethix analysis shows this shift risks reversing years of progress, where Pennsylvania’s uninsured rate had dipped to 5.4% or about 677,600 people before the changes.

Real-world impacts already appear in hospital systems facing higher uncompensated care. Forecasts suggest that rural Pennsylvania healthcare facilities are likely to experience a loss of millions in revenue, concurrent with a sharp increase in uncompensated care costs. This situation generates a cascading impact throughout the healthcare economy, imposing significant stress on providers and consequently elevating expenses for all insured individuals.

High-authority modeling from sources like KFF and Urban Institute predicts up to 4.8 million additional uninsured Americans nationally if trends hold. In Pennsylvania, the 120,000 drop represents one of the largest state-level hits, with 104,000 confirmed early in the year and more expected as bills come due. Carethix views this as a business wake-up call for insurers, employers, and policymakers to innovate fast.

The case underscores how subsidy loss intersects with daily economic pressures. Families report skipping prescriptions or routine checkups to save money. Yet targeted solutions exist to rebuild coverage without waiting for federal action.

Carethix Critique: Risks, Gaps, and Systemic Failures Exposed by ACA Subsidy Loss

Carethix views the sudden expiration of the enhanced ACA subsidies as a significant policy error, one that disregards both established public support and fundamental economic factors. The fact that premiums for middle-income families could double almost instantly, creating an unmanageable “affordability cliff” evidenced by the 120,000 people who lost coverage in Pennsylvania, demonstrates the decision’s immediate harm. This move does not address systemic issues, such as the underlying escalation of medical costs, but instead deepens existing vulnerabilities within the healthcare system.

Risks emerge quickly in delayed care and worsening health outcomes. Uninsured individuals turn to emergency rooms more often, driving up system-wide costs by billions. Pennsylvania hospitals already project significant increases in uncompensated care, threatening rural closures and longer wait times for insured patients.

Gaps in the original ACA framework become glaring without subsidy support. Tax credits are still accessible, but their value has significantly diminished. Individuals earning over 400% of the poverty level must now bear the full cost. The abrupt loss of these subsidies, known as the “cliff effect,” disproportionately impacts states like Pennsylvania, where the rise in the cost of living has outpaced wage increases, according to analysis by Carethix.

Broader risks include medical bankruptcies and reduced workforce productivity. National estimates point to 4.8 million more uninsured, with Pennsylvania contributing disproportionately through its 102% premium spike. The critique centers on missed opportunities for bipartisan extensions despite widespread popularity in polls.

Political and structural gaps compound the problem. Congress failed to act despite House votes and public demand, prioritizing short-term budget concerns over long-term stability. Carethix warns this approach burdens state budgets and safety-net providers while eroding gains in coverage achieved since 2021.

The pain point of skyrocketing costs without relief creates a false choice between insurance and essentials. Families report sacrificing food for utilities in surveys, aggravating chronic health issues like diabetes and hypertension. Systemic failures leave those ineligible for Medicaid expansion or employer plans without easy alternatives.

Carethix calls out the lack of transitional support as shortsighted. Without bridges like state-funded aid or innovative private options, enrollment erosion will accelerate. This critique demands accountability from leaders to close these vulnerabilities before they deepen.

Solutions: Strategic Pathways to Restore Affordable Coverage and Business Stability

Carethix provides actionable remedies for the 120,000 Pennsylvania residents losing Affordable Care Act coverage, implementing immediate adjustments and comprehensive long-term strategies. Individuals retain the ability to utilize any remaining Pennie premium tax credits during forthcoming special enrollment periods, facilitating a comparison of plans to identify judicious, cost-effective Silver or Bronze tier options that effectively limit maximum out-of-pocket expenditures.

Employers gain leverage by expanding group health plans or offering stipends for marketplace coverage. Small businesses in Pennsylvania qualify for tax credits under the ACA that offset up to 50% of premiums, easing the burden on owners and employees alike. Carethix recommends bundling wellness programs to lower claims and attract talent in competitive markets.

Providers and insurers must innovate with value-based care models that reward prevention over volume. Telehealth partnerships cut costs by 30 to 50% for routine visits while expanding access in rural areas hit hardest by drops. Direct primary care memberships provide unlimited visits for flat monthly fees, bypassing traditional insurance hurdles.

High-deductible health plans, which remain an option in the marketplace, are effectively complemented by financial instruments such as Health Savings Accounts (HSAs). These accounts grow tax-free and cover deductibles, offering a buffer against the 102% premium hikes. Carethix advises clients to maximize contributions up to IRS limits for 2026 to build immediate savings.

State-level options include exploring Pennsylvania’s reinsurance program effects and any new assistance pilots. Short-term limited-duration insurance fills gaps for those between jobs, though with coverage limits. Carethix guides businesses toward association health plans that pool risks for lower group rates.

Technology solutions streamline enrollment and cost transparency. Apps and navigators from Pennie help families model scenarios and find qualifying events for special enrollment. For healthcare organizations, data analytics identify at-risk patients early, reducing uncompensated care spikes projected at billions nationally.

Partnerships between hospitals and community clinics create safety nets that absorb some drops without full insurance. Negotiating payment plans or charity care policies minimizes medical debt fallout. Carethix business analysis shows these steps preserve revenue streams while fulfilling mission-driven care.

These solutions integrate effective policy management with the dynamic capabilities of the private sector. By taking immediate action, Pennsylvania stakeholders can mitigate the projected 120,000 losses and prevent further regression toward the pre-subsidy uninsured baseline of 677,600. Carethix is prepared to implement tailored strategies that yield demonstrable return on investment.

Prevention: Proactive Steps to Shield Against Future Healthcare Affordability Crises

Carethix focuses on prevention to avert repeat scenarios like the 120,000 ACA drop. Layered safeguards and forward planning are key. Personal emergency health funds covering three to six months of premiums will shield families from abrupt subsidy changes. Regular income reviews ensure eligibility for any remaining credits or Medicaid adjustments as circumstances change.

Businesses prevent exposure by diversifying benefits with multiple plan tiers and employee education sessions. Annual wellness audits identify cost drivers early, cutting claims by up to 20% through targeted interventions. Carethix recommends scenario modeling for subsidy cliffs to adjust compensation packages proactively.

Policy advocacy at state and local levels pushes for Pennsylvania-specific reinsurance expansions or mini-subsidies funded through existing budgets. Engaging congressional representatives keeps pressure on for future extensions, given the subsidies’ prior success in boosting enrollment to 24 million nationally.

Provider networks invest in cost-containment technologies like AI-driven utilization management to lower overall premiums long-term. Community education campaigns on marketplace navigation reduce drop rates by empowering informed choices before open enrollment ends. Carethix tracks legislative calendars to alert clients of windows for input.

Hospitals can build resilience against the national estimated $2.2 billion rise in uncompensated care by strategically diversifying their revenue. This diversification can be achieved through expanding outpatient services and forming partnerships with telehealth companies. Rural facilities gain resilience via shared service models that spread fixed costs. Prevention here means turning vulnerability into sustainable operations.

Individual habits like prioritizing preventive screenings under ACA-mandated free coverage catch issues early and avoid expensive emergencies. Health literacy programs from employers reinforce these behaviors, fostering a culture of proactive wellness. Carethix integrates these into client strategies for lasting impact.

Monitoring economic indicators such as inflation and wage growth helps forecast affordability risks. Flexible work arrangements that include benefits portability prevent coverage gaps during job transitions. These measures establish a robust ecosystem with reduced susceptibility to future shocks induced by subsidies.

By embedding prevention into daily operations and personal finance, stakeholders avoid the 102% premium pain seen in 2026. Carethix views this as essential risk management that protects both health outcomes and bottom lines across Pennsylvania’s healthcare landscape.

Carethix Key Takeaways: Our Expert Opinion on Healthcare Resilience

The 120,000 Pennsylvania ACA drops demand bold, immediate action from Carethix, not passive hope for federal fixes. Subsidies alone are insufficient; coverage requires simultaneous innovation in cost control and access. Businesses and families who adapt now will thrive while others lag.

We assert that blending marketplace navigation with private alternatives like direct care and HSAs delivers faster relief than waiting for policy reversals. Data on doubled premiums and rising uncompensated care leaves no room for delay. Proactive strategies transform threats into opportunities for stronger, fairer healthcare delivery.

In our expert view, prevention through education, diversification, and advocacy must become standard practice. Pennsylvania’s experience highlights national vulnerabilities that smart consultancies like Carethix can help resolve. Resilience starts with informed choices today.

Carethix emphasizes that affordability must be a fundamental business and personal priority for all stakeholders. By strategically managing premium costs, we can restore coverage for thousands and construct a healthcare system prepared for future challenges. Immediate action is essential.

Reference – 120,000 Pennsylvanians have dropped ACA health insurance since the loss of federal subsidies