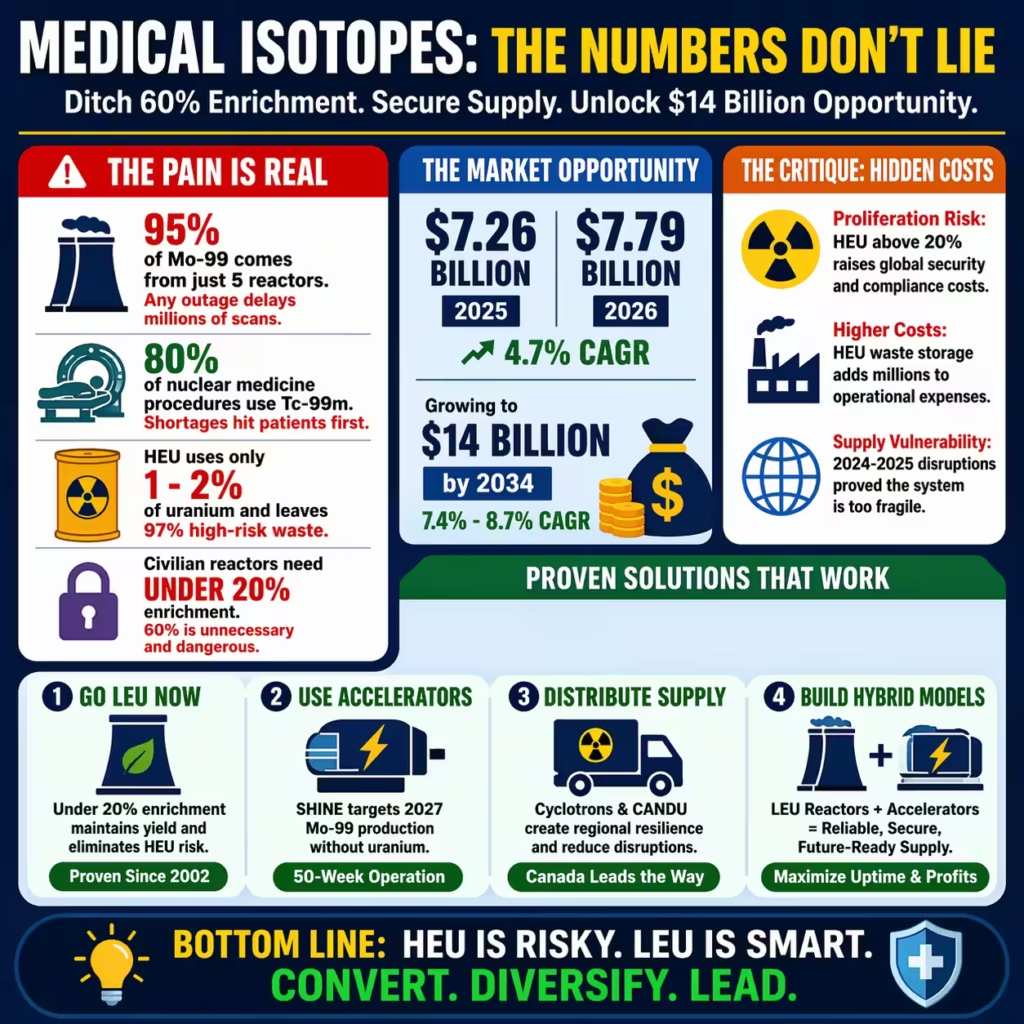

Civilian research reactors need under 20% uranium enrichment for medical isotopes, yet 60% enrichment remains unjustified in some operations worldwide. This practice directly fuels proliferation risks and supply fragility in the global medical isotopes market valued at $7.26 billion in 2025 and projected to hit $7.79 billion in 2026. Carethix consultants see immediate solutions through low-enriched uranium conversion and accelerator technologies that slash security costs while unlocking reliable profits for healthcare providers and manufacturers.

The pain hits hardest in the molybdenum-99 supply chain that feeds technetium-99m used in 80% of nuclear medicine procedures. Five major reactors currently produce 95% of global Mo-99, and any outage triggers shortages that delay millions of scans annually. Recent data from 2025 shows persistent vulnerabilities, with facilities like Belgium’s BR2 still planning HEU phase-out only by 2026 despite proven LEU alternatives available since 2018 in the Netherlands and South Africa.

Real-world numbers underscore the inefficiency. Producers using high-enrichment targets consume only 1 to 2% of the uranium while generating radioactive waste that requires costly secure storage. Iran’s Tehran Research Reactor example illustrates the issue, where 60% enriched uranium targets yield small medical outputs yet add unnecessary proliferation exposure. Market forecasts indicate the radioactive medical isotopes segment alone will grow from $5.8 billion in 2025 to $6.3 billion in 2026 at 4.7% CAGR, yet outdated enrichment drags down margins.

Carethix analysis reveals that full LEU adoption could stabilize supply without sacrificing yield quality. Countries like Australia with OPAL reactors have used LEU targets successfully for years, delivering consistent output at lower security overhead. Business leaders who convert now position themselves ahead of tightening IAEA safeguards and U.S. NNSA incentives for domestic production.

The financial upside is clear in a market expanding at 7.4 to 8.7% CAGR through 2034. New projects such as SHINE Technologies’ accelerator-based Mo-99 facility slated for 2027 operation promise redundancy without uranium enrichment entirely. Healthcare systems dependent on just-in-time isotope delivery face daily losses during disruptions exceeding millions, making diversification a profit imperative rather than a compliance burden.

Recent OECD NEA reports from 2025 highlight how COVID-era travel restrictions exposed the fragile air-transport logistics for short-half-life isotopes. Civilian reactors operating below 20% enrichment already meet all technical needs for fission-based production. Forward-thinking operators who adopt these methods gain competitive edges through reduced insurance premiums and enhanced investor appeal in an ESG-focused funding landscape.

Carethix Critique: Risks, Gaps, and Hidden Costs of 60% Enrichment Practices

High-enrichment uranium at 60% creates unacceptable proliferation and terrorism risks in civilian medical isotope production. Carethix consultants flag that even small annual HEU volumes, such as the 20 kilograms historically imported by one major supplier, leave 97% unused in waste vulnerable to diversion. This gap undermines global nuclear security while inflating operational expenses in a $7 billion-plus market facing 2025 supply volatility.

The pain point intensifies with regulatory and reputational exposure. Facilities still reliant on HEU face potential export restrictions and higher safeguarding costs under IAEA protocols that classify material above 20% as high-risk. Recent 2025 data shows only partial global conversion progress, with Russia and select reactors continuing HEU targets despite LEU technical feasibility proven in Argentina since 2002 and multiple European sites by 2023.

Gaps in current practices include technical yield reductions during LEU transitions that raise short-term processing costs by 20 to 50%. Yet these pale against long-term security liabilities, as HEU waste requires specialized storage that adds millions annually to balance sheets. Geopolitical tensions further amplify risks, with transport disruptions already causing 2024-2025 shortages in Tc-99m formulations listed by major hospital networks.

Carethix identifies over-reliance on five aging reactors as a critical vulnerability that 60% enrichment exacerbates. Outages at the High Flux Reactor have repeatedly forced procedure cancellations across Europe and North America. This model fails modern healthcare demands where nuclear medicine supports rising cancer and cardiac diagnostics projected to drive 8.71% CAGR to $14 billion by 2034.

Public and investor scrutiny grows as proliferation concerns link civilian programs to broader security debates. Hospitals and radiopharma firms risk brand damage when supply chains trace back to unjustified high-enrichment methods. The critique is clear: continuing 60% practices is not only technically unnecessary but financially reckless in a sector where resilience directly correlates with market share.

| Related Analysis: $2.7M Health Renovation: Smart ROI Solutions 150% More Cancer Risk from Pesticides: Safer Agri Strategies 500 Outreach Cases Reveals Scalable Healthcare Opportunity |

Solutions: Proven Pathways to Low-Enrichment and Alternative Isotope Production

Low-enriched uranium conversion provides the fastest solution for existing reactor-based production. Carethix recommends full target and fuel shifts to under 20% enrichment, as successfully completed by Curium Pharma in 2018 and IRE in early 2023. These transitions maintain medical isotope output while eliminating HEU security overhead and aligning with 2025 OECD resilience strategies.

Accelerator and cyclotron technologies offer uranium-free alternatives that bypass enrichment entirely. SHINE’s Chrysalis fusion accelerator targets 2027 commercial Mo-99 output with 50-week operation cycles and built-in redundancy. NorthStar’s electron accelerator method already demonstrates minimal waste using enriched molybdenum-98 targets, providing scalable domestic supply that cuts transport risks in the $7.26 billion 2025 market.

Solution irradiation and non-fission routes further diversify production. Canada’s CANDU reactors now integrate Lu-177 output without dedicated isotope facilities, doubling capacity from 2022. TRIUMF’s direct Tc-99m cyclotron production received Health Canada approval in 2020 and scales without reactor dependency. These methods address 95% supply concentration by enabling distributed manufacturing closer to end users.

Business integration of these solutions drives profitability through vertical partnerships. Radiopharma companies like Novartis expanded U.S. facilities in 2024 to counter shortages, demonstrating ROI from localized production. Carethix advises healthcare leaders to secure offtake agreements with new 2027-2030 projects such as PALLAS reactor and Argentina’s RA-10 expansion for guaranteed volumes at predictable pricing.

Investment in hybrid models combines LEU reactors with accelerator backups for ultimate resilience. Poland’s MARIA reactor enhancements and emerging U.S. initiatives under NNSA support create funding opportunities that lower capital barriers. Early adopters capture market share as therapeutic isotopes like Lu-177 and Ac-225 grow faster than diagnostics at 11.45% CAGR segments.

Regulatory navigation and workforce upskilling complete the solution set. Dual GMP and nuclear licensing frameworks demand streamlined approvals that Carethix helps clients achieve through compliance roadmaps. Training programs for radiochemists and hot-cell operators ensure operational readiness, turning technical challenges into competitive advantages in a sector forecast to reach $14 billion by 2034.

Prevention Steps: Safeguarding Future Medical Isotope Supply Against Enrichment and Disruption Risks

International collaboration establishes standardized LEU conversion timelines to prevent future gaps. Carethix urges healthcare executives to advocate for expanded NEA and IAEA frameworks that incentivize complete HEU phase-outs by 2030. Reserve capacity agreements modeled on 2025 OECD recommendations ensure outage coverage without reverting to high-enrichment methods.

Domestic production mandates reduce geopolitical exposure in supply chains. U.S. and European policy support for accelerator facilities like SHINE creates buffers against the five-reactor dominance that caused 2024-2025 shortages. Prevention includes government-backed financing for new projects targeting 300 operational days annually, directly supporting the projected 8.4% CAGR in isotope production through 2040.

Technology monitoring and R&D investment block regression to outdated practices. Continuous assessment of high-assay low-enriched uranium developments for advanced reactors keeps options open while prioritizing under-20% civilian applications. Carethix recommends annual supply-demand forecasting to match emerging radioligand therapies with resilient production pipelines.

Workforce and infrastructure resilience programs form the final prevention layer. Dedicated training initiatives address radiopharmacy personnel shortages that compound facility constraints. Hospital networks should build on-site generators and diversified supplier contracts to maintain procedure continuity even during global disruptions.

Policy advocacy for reimbursement alignment accelerates adoption of preventive measures. Updated frameworks that value supply security in pricing models encourage investment in LEU and non-reactor technologies. These steps collectively protect the $7 billion-plus market from repeating past vulnerabilities while positioning participants for sustained growth.

Carethix Key Takeaways: Act Decisively to Own the Safer, More Profitable Isotope Future

The era of unjustified 60% enrichment must end immediately. Carethix’s opinion is unambiguous: healthcare leaders who delay LEU conversion or accelerator adoption risk regulatory exclusion, security breaches, and lost market share in a sector growing to double digits by 2034. You hold the power to transform risks into revenue by embracing under-20% solutions today.

Proactive investment in diversified production yields unmatched returns. Early movers securing SHINE, PALLAS, and CANDU partnerships lock in stable supply at lower long-term costs while enhancing ESG credentials that attract capital. The data from 2025 conversions proves technical feasibility and profit upside far outweigh transition expenses.

Your next move defines competitive advantage. Demand LEU commitments from suppliers, fund domestic accelerator capacity, and integrate resilience into every strategic plan. Carethix stands ready to guide implementation that safeguards patients, secures profits, and strengthens global health security for decades ahead. The $7 billion isotope opportunity rewards only the bold who act now.

Reference – Less than 20% Uranium enrichment needed for Medical Isotopes