ACA’s 5M coverage crisis demands a strategic retention roadmap to protect risk pools and stabilize revenues.

Case Study: The 2026 Subsidy Cliff and Market Destabilization

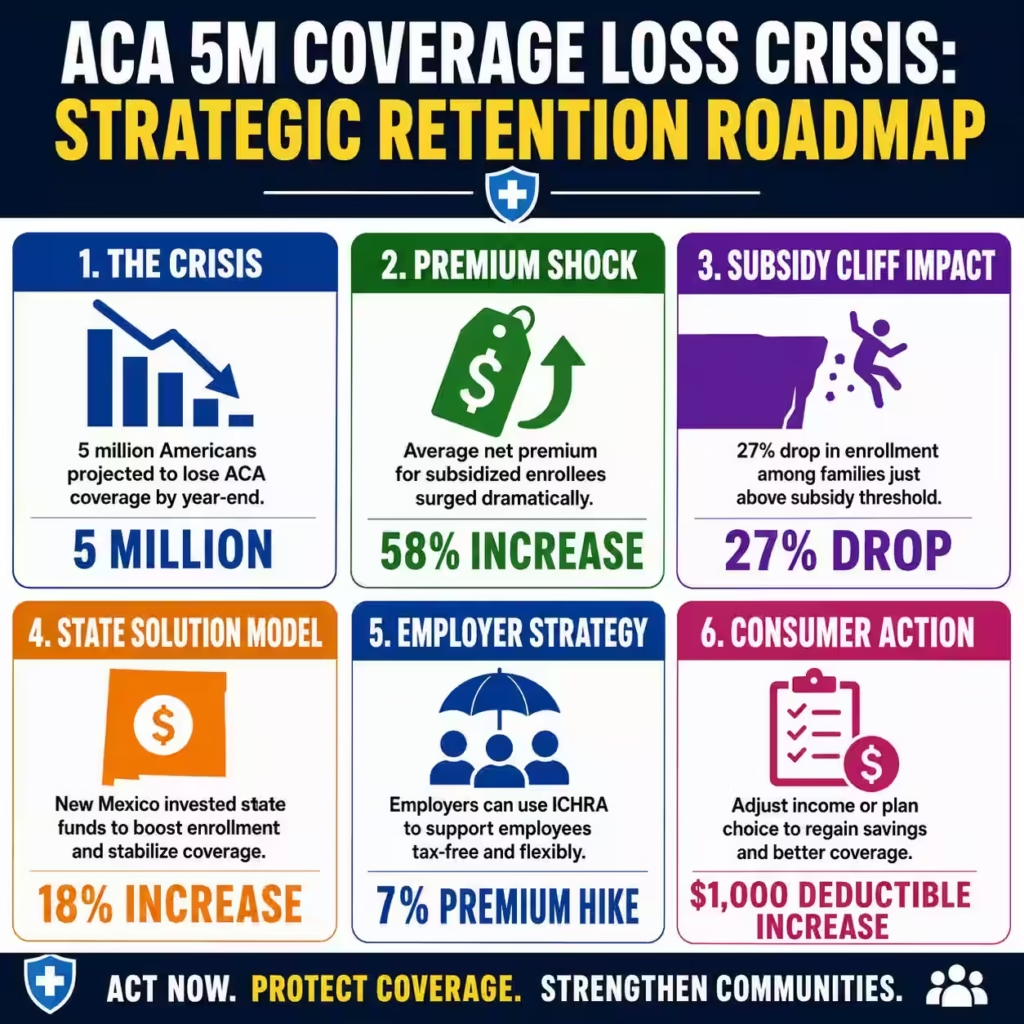

Six months after the expiration of enhanced Affordable Care Act (ACA) subsidies, the healthcare landscape faces its most severe destabilization since the program’s inception. The administration initially reported a decline of 1.5 million sign-ups in January 2026, a figure that severely understates the unfolding crisis as premiums for benchmark silver plans surged by 21.7% overnight. This reduction in federal support has exposed more than 20 million Americans to sudden premium hikes, with average net premiums jumping 58% to $178 per month for subsidized enrollees.

The initial 5% drop in open enrollment—1.2 million fewer selections than in 2025—was merely the leading edge of a larger attrition wave driven by affordability challenges. Independent analyses from KFF and Wakely Consulting Group now project that total effectuated enrollment will plummet by approximately 5 million people by year’s end, dropping from a high of 22.3 million to roughly 17.5 million. This attrition is most acute among middle-income families earning between 400% and 600% of the federal poverty level, who have fallen off the “subsidy cliff” and now face the full, unsubsidized cost of care.

State-level data corroborates this accelerating decline, with Maryland reporting a 13% drop and Arkansas seeing a 16% decrease in active coverage between January and April 2026. Conversely, New Mexico defied this national trend by allocating $40 million in state funds to replace lost federal credits, resulting in an 18% enrollment increase and proving that financial policy, not consumer disinterest, drives these fluctuations. The “phantom” menace is not the presence of fake enrollees, but the very real disappearance of affordable coverage for millions of working families.

Carethix Critique: The False Narrative of “Phantom” Enrollees

The political narrative characterizing the ACA marketplace as bloated with “fake enrollees” fundamentally misdiagnoses the structural reality of the 2026 health insurance market. Critiques focusing on enrollment integrity ignore the verifiable economic pain inflicted on 22 million legitimate consumers who utilized enhanced subsidies to maintain essential health security. By framing the subsidy expiration as a correction of waste, policymakers have effectively sanctioned a tax increase on the sick and middle class, driving the uninsured rate upward for the first time in five years.

This rhetorical strategy masks the profound risk shift occurring within the insurance risk pools, as healthy, younger individuals exit the market in disproportionate numbers. Adults aged 18-34 showed the lowest sign-up rates in 2026, leaving a smaller, sicker, and costlier pool of insured individuals that will inevitably drive premiums even higher for 2027. The “phantom” argument fails to account for the 27% enrollment drop among those earning just above the subsidy threshold, a demographic that is demonstrably real and financially vulnerable.

Carethix analysis indicates that the removal of enhanced tax credits has not eliminated fraud, but rather eliminated choice for financially strapped households. Enrollees have been forced to migrate to “skimpier” bronze plans or short-term coverage, evidenced by the average marketplace deductible skyrocketing by $1,000 to nearly $3,800 in 2026. This degradation of coverage quality creates a “phantom” insurance product—one that technically counts as enrollment but provides little financial protection against actual medical emergencies.

The systemic gap identified here is a failure to recognize healthcare stability as a pillar of economic productivity. When 5 million Americans lose coverage, the downstream effects on hospital bad debt and uncompensated care will eventually force provider rates higher for the entire commercial market. We are witnessing a manufactured crisis where the removal of a fiscal stabilizer—the enhanced premium tax credit—has reintroduced volatility into a previously stabilizing market.

Strategic Solutions for Stakeholders and Consumers

Immediate State-Level Intervention Protocols

State legislatures must immediately evaluate the “New Mexico Model” of appropriating emergency funds to bridge the federal subsidy gap for the remainder of the fiscal year. Data confirms that state-funded wrap-around subsidies can completely neutralize the adverse effects of federal inaction, preserving the risk pool and maintaining enrollment levels. Insurance commissioners in affected states should aggressively pursue Section 1332 waivers to implement reinsurance programs that directly lower premiums for unsubsidized enrollees.

Employer-Sponsored Alternative Coverage

Employers currently facing their own 7% premium increases must leverage Individual Coverage Health Reimbursement Arrangements (ICHRA) to offer tax-advantaged support to employees priced out of the group market. An ICHRA allows businesses to reimburse employees for individual premiums tax-free, effectively creating a private subsidy system that bypasses federal gridlock. This approach empowers employees to shop for plans that fit their specific budget while insulating the employer from catastrophic claims risk.

Consumer Portfolio Rebalancing

Individuals facing the “subsidy cliff” must immediately reassess their household income projections to determine if they qualify for cost-sharing reductions (CSR) by adjusting contributions to 401(k) or HSA accounts. Reducing Modified Adjusted Gross Income (MAGI) can sometimes bring a household back under the 400% poverty line, restoring eligibility for significant federal assistance. Consumers should also investigate “Silver Loading” dynamics in their specific zip code, where silver plan premiums may be disproportionately high, making Gold plans surprisingly more affordable.

Health System Revenue Cycle Adaptation

Hospitals and provider networks must urgently revise their charity care policies and self-pay discount schedules to accommodate the surge in underinsured patients facing $3,800 deductibles. Revenue cycle teams should implement up-front financial counseling to connect patients with catastrophic coverage or third-party foundation assistance before scheduled procedures. Proactive financial triage is now a clinical necessity to prevent a deluge of uncollectible bad debt from the newly uninsured population.

Broker and Navigator Redeployment

Health insurance brokerages must pivot their outreach strategy to target the “young invincibles” (ages 18-34) with catastrophic plan options that prevent total market exit. Navigators need to be retrained to identify clients eligible for Medicaid expansion or special enrollment periods triggered by life events, ensuring no eligible individual remains uninsured due to administrative complexity. Preserving the risk pool requires a microscopic focus on retaining every possible healthy life within the insured ecosystem.

Prevention Methodologies for Future Market Stability

Legislative Risk Corridor Implementation

To prevent future “cliffs,” federal or state policy must establish permanent risk corridors that automatically trigger subsidy adjustments based on premium volatility indices. Linking subsidy thresholds to a percentage of income rather than an arbitrary poverty line multiplier ensures that coverage remains affordable regardless of inflationary pressure. This structural fix effectively “pandemic-proofs” the insurance market against future economic shocks or legislative stalling.

Diversification of Risk Pools

Insurers must innovate beyond the ACA exchange model by integrating off-exchange products that pool individual risk with small group associations. Creating broader risk pools that include gig economy workers and freelancers can dilute the impact of high-cost claimants and reduce reliance on direct government subsidies. This prevention strategy moves the market toward actuarial sustainability rather than perpetual political dependency.

Mandatory Financial Literacy Integration

Healthcare literacy must be elevated to a primary preventative measure, educating consumers on the mechanics of MAGI optimization and the long-term cost of short-term plans. State exchanges should mandate a “financial health check” module during enrollment that visually demonstrates the trade-off between lower premiums and higher deductibles. Informed consumers are statistically less likely to drop coverage during price shocks, providing a stabilizing inertia to the market.

Value-Based Insurance Design (VBID) Adoption

Payers and regulators should accelerate the adoption of VBID principles that exempt high-value services—such as insulin and cardiac maintenance drugs—from deductibles entirely. By ensuring that essential care remains accessible even in high-deductible plans, we prevent the medical deterioration of enrollees that leads to explosive costs later. This approach maintains the clinical value of insurance even when financial protection is eroded by subsidy loss.

Algorithmic Enrollment Retention

Exchanges must deploy predictive analytics to identify enrollees at high risk of lapsing due to premium hikes before the termination date. Automated, personalized intervention campaigns can offer alternative plan mappings or financial restructuring advice to retain these members. Preventing churn at the individual level aggregates into macro-level market stability.

Carethix Key Takeaway

The 2026 healthcare market contraction is not a failure of the Affordable Care Act’s architecture, but a predictable consequence of withdrawing its foundational financial pillars. The data is unequivocal: where subsidies vanished, 5 million Americans followed; where states like New Mexico intervened, coverage expanded. The “phantom menace” rhetoric serves only to distract from the tangible economic damage inflicted on the 20 million Americans now paying 58% more for essential security.

We are effectively witnessing a controlled demolition of the individual market’s risk pool, driving a wedge between the healthy and the sick that will reverberate through 2027 premium cycles. The shift toward higher deductibles represents a “hollowing out” of coverage, transforming insurance into a catastrophic safety net rather than a tool for health maintenance. This regression threatens to erase a decade of progress in reducing uncompensated care and stabilizing provider revenues.

Carethix advises all stakeholders to abandon the expectation of a federal rescue and immediately pivot toward state-based, employer-driven, and individual financial strategies. The future of American healthcare security now relies on decentralized innovation and the aggressive management of personal financial risk. In this volatile environment, passivity is the only guarantee of insolvency.