India’s $124.5B diagnostics surge exposes scalability risks—strengthen your lab growth with smarter expansion.

The Indian Diagnostics Landscape: A Multi-Billion Dollar Shift

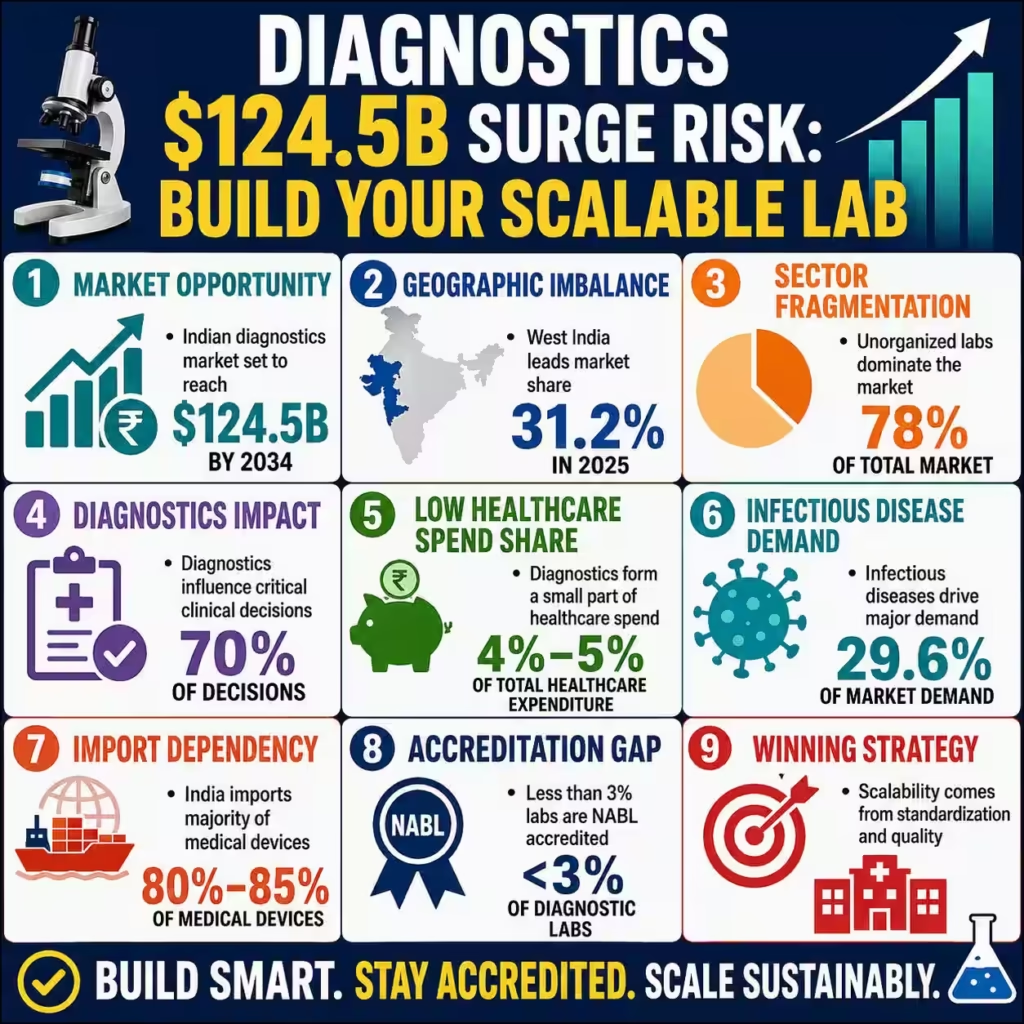

The Indian diagnostic market is projected to reach USD 124.5 billion by 2034, driven by expanding government-backed healthcare initiatives, continuous innovation in molecular diagnostics, and rapid digital health adoption across underserved tier-2 and tier-3 markets. However, this accelerating market growth exposes a critical structural bottleneck, as high-quality infrastructure and standardized testing services remain disproportionately concentrated in affluent metropolitan areas while rural providers struggle with access. To successfully capture this massive market expansion, forward-looking enterprise operators must urgently transition toward standardized hub-and-spoke logistics, digital sample tracking systems, and diversified, high-margin preventive wellness portfolios.

Historical data from the IMARC Group reveals that West India commanded a leading 31.2% share of the diagnostics market in 2025, primarily driven by a dense concentration of tier-1 corporate hospitals, robust private-sector investments, and advanced laboratory infrastructure in Maharashtra and Gujarat. This profound geographic imbalance leaves nearly 70% of the national population residing in rural or semi-urban districts with highly variable access to standardized clinical pathways and reliable pathology services. The diagnostic segment currently influences approximately 70% of all critical clinical decisions in the country, yet it historically represents a mere 4% to 5% of the total national healthcare expenditure.

While major national diagnostic chains like Dr. Lal PathLabs and Metropolis Healthcare aggressively expanded their physical footprints by adding hundreds of new collection centers in 2025, the overall sector remains extensively fragmented. Unorganized, independent laboratories still account for nearly 78% of the total market, operating with highly variable quality control protocols, inconsistent technician training, and minimal regulatory oversight. The rapid expansion of organized chains, which grew their combined market share from 15% to 22% by fiscal year 2024, signals an inevitable shift toward institutional consolidation and corporate brand preference.

This consolidation pressure is compounded by the rising prevalence of complex chronic conditions, which require continuous patient monitoring and sophisticated clinical pathology panels. Furthermore, infectious disease diagnostics continue to dominate the application segment, representing nearly 29.6% of the overall market demand due to seasonal disease outbreaks and dense urban populations. As a result, clinical chemistry and reagent kits constitute approximately 67.4% of product-type revenues, reflecting the exceptional transactional volume of routine medical testing protocols across urban and rural centers.

Institutional private capital is actively seeking to exploit these high-growth dynamics, with healthcare-focused venture funds injecting substantial capital into digital-first testing platforms and remote home collection apps. However, many of these digital aggregators rapidly burn through capital by offering deeply discounted packages without establishing the physical laboratory infrastructure required to ensure clinical accuracy. This severe operational mismatch creates dangerous quality discrepancies across test reports, threatening patient outcomes and undermining broader physician trust in digital healthcare portals.

Forward-thinking healthcare executives must realize that pure volume expansion without standardized quality controls is a fundamentally unsustainable business model in this maturing market. The upcoming decade will heavily reward enterprise operators who strategically balance geographic expansion into semi-urban districts with strict clinical governance and international accreditations. By aligning corporate expansion strategies with India’s expanding digital public infrastructure, diagnostic providers can establish durable market dominance and secure highly predictable institutional financial returns.

The Carethix Industry Critique: Risks, Fragmentation, and Gaps

The projected expansion of the Indian diagnostic sector obscures several systemic risks that healthcare executive leadership teams must immediately address to prevent operational failure. Chief among these critical vulnerabilities is the stark geographical disparity, exemplified by the reality that West India captured over 31% of the total market share in 2025. This heavy concentration of advanced laboratories and private equity capital in wealthy western states leaves vast territories in East and North-East India completely starved of modern pathology infrastructure and advanced clinical testing.

In addition to severe geographic inequity, the diagnostic sector suffers from a critical lack of standardized quality regulation across its estimated 100,000 independent testing establishments. According to official data from the National Accreditation Board for Testing and Calibration Laboratories, less than 3% of all active diagnostic facilities in India possess official clinical accreditation. This regulatory void allows thousands of unaccredited labs to issue critical clinical reports daily, resulting in high diagnostic error rates, inconsistent therapeutic pathways, and compromised patient safety.

Another major systemic risk is the severe dependency of the Indian medical diagnostics sector on imported machinery and raw chemical reagents. India currently imports approximately 80% to 85% of its medical devices, advanced imaging systems, and high-end molecular diagnostic instruments from multinational manufacturers. This extensive dependency exposes domestic laboratory operators to severe currency fluctuations, high import duties, and global supply chain disruptions that directly threaten operating margins.

Furthermore, aggressive price wars initiated by venture-backed digital health aggregators have triggered severe margin compression across traditional, brick-and-mortar diagnostic networks. These online portals frequently market comprehensive wellness packages at unsustainably steep discounts, forcing quality-conscious laboratory networks to lower their rates to retain essential market share. While these aggressive customer acquisition tactics yield short-term volume increases, they ultimately starve the broader diagnostic ecosystem of the capital reserves required to purchase modern clinical instruments.

The rapid expansion of complex diagnostic networks into remote tier-2 and tier-3 markets is also severely bottlenecked by a critical shortage of certified laboratory technicians and qualified pathologists. Operationalizing advanced molecular assays and gene sequencing platforms in rural districts remains practically impossible without a dedicated local workforce trained to operate high-throughput machinery. Consequently, many decentralized collection points and processing hubs operate under the supervision of undertrained staff, escalating the probability of sample contamination and catastrophic clinical errors.

Finally, the rapid digital health integration celebrated in optimistic industry reports presents severe cybersecurity and patient data privacy vulnerabilities. Most regional diagnostic chains operate on obsolete laboratory information systems that completely lack modern encryption standards or robust defense firewalls. This severe technological neglect exposes millions of sensitive patient clinical records to malicious ransomware syndicates and unauthorized commercial monetization by third-party data brokers.

Strategic Operational and Financial Solutions for Market Expansion

To successfully mitigate these severe systemic risks and capitalize on the projected market expansion, diagnostic enterprises must deploy an optimized, tiered hub-and-spoke operational architecture. Under this structured operational framework, highly complex molecular assays, advanced oncology profiling, and sophisticated genetic sequencing are centralized in fully accredited, state-of-the-art reference laboratories located in major metropolitan areas. Simultaneously, lower-cost, rapid-turnaround basic clinical pathology services are distributed across smaller, regional satellite laboratories and localized sample collection points situated closer to the patient populations.

This tiered operational configuration must be supported by advanced Internet of Things temperature monitoring sensors integrated directly into the biological sample logistics network. Maintaining strict cold-chain integrity during sample transport from remote tier-3 rural clinics to centralized urban processing facilities prevents specimen degradation and eliminates costly pre-analytical diagnostic errors. Real-time GPS and temperature tracking software ensures that diagnostic operators can monitor sample conditions continuously, optimizing routing logistics and significantly reducing clinical turnaround times.

From a strategic financial perspective, diagnostic operators must shift toward an asset-light corporate franchising model to accelerate geographic expansion without exhausting liquid capital reserves. By partnering with local medical entrepreneurs who fund the physical real estate acquisition and basic administrative setup, national diagnostic chains can rapidly penetrate underserved secondary markets. This collaborative expansion strategy successfully distributes the heavy capital expenditure requirements of physical growth while ensuring absolute compliance with standardized corporate clinical protocols and quality controls.

To effectively resolve the geographic concentration of services, healthcare enterprises should actively participate in structured public-private partnerships with state and local governments. Under these formal contractual agreements, municipal governments provide subsidized physical spaces within public hospitals, and private operators deliver high-quality pathology services at standardized, pre-negotiated rates. This symbiotic business model secures a guaranteed and steady patient volume for commercial diagnostic operators while offering rural populations immediate access to reliable, clinically validated testing.

Diagnostic corporations must also aggressively implement digital pathology platforms and artificial intelligence analytical tools to successfully combat the acute global shortage of certified pathologists. Digital slide scanners can effortlessly convert physical tissue samples into high-resolution electronic images that are instantly transmitted to centralized medical specialists located in major urban centers. Concurrently, validated artificial intelligence software can pre-screen routine clinical slides to flag obvious cellular abnormalities, drastically reducing the manual diagnostic workload of onsite medical professionals.

Finally, progressive diagnostic providers must strategically transition their clinical portfolios away from commoditized routine tests and toward personalized, premium-priced preventive wellness packages. Customizing diagnostic panels for chronic lifestyle disorders such as advanced diabetes, cardiovascular diseases, and complex metabolic syndromes provides corporate clients with invaluable preventative healthcare solutions. This clinical shift not only improves retail customer retention through longitudinal health tracking but also establishes a predictable, recurring corporate revenue stream for the parent enterprise.

Prevention Measures for Future Operational and Structural Failures

To prevent catastrophic clinical errors and ensure long-term operational resilience, diagnostic enterprises must establish comprehensive, mandatory quality assurance protocols across all testing facilities. Implementing standardized internal quality controls and enrolling in robust external quality assessment schemes ensures that analytical instruments maintain peak accuracy under high workload stress. Obtaining and maintaining prestigious national accreditations, such as the National Accreditation Board for Testing and Calibration Laboratories certification, serves as a vital safeguard against clinical reporting errors.

To prevent severe margin compression stemming from international supply chain dependencies, diagnostic operators must negotiate long-term procurement contracts with integrated currency hedging clauses. Establishing strategic, multi-year supply agreements with international medical device manufacturers locks in reasonable equipment prices and protects laboratories from sudden macroeconomic volatility. Additionally, operators should diversify their supply chains by actively vetting and onboarding emerging domestic diagnostic manufacturers that produce high-quality reagents and instruments within the country.

Preventing devastating diagnostic data breaches and securing highly sensitive patient electronic medical records requires the immediate deployment of advanced cybersecurity frameworks and zero-trust security architectures. Enforcing strict multi-factor user authentication, end-to-end database encryption, and regular external vulnerability assessments successfully protects corporate diagnostic networks from sophisticated ransomware syndicates. Furthermore, establishing clear corporate data governance policies ensures total compliance with evolving national digital health privacy regulations, thereby avoiding severe financial penalties and irreparable brand reputation damage.

To mitigate critical workforce shortages and prevent operational disruptions, diagnostic chains must invest heavily in proprietary technical training academies and continuous professional education. Establishing specialized training institutions allows diagnostic firms to develop a steady pipeline of competent laboratory technicians, phlebotomists, and quality managers directly in secondary markets. Offering structured career progression pathways, competitive financial incentives, and modern technical upskilling opportunities effectively minimizes staff turnover and maintains operational consistency.

Diagnostic enterprise networks must also execute rigorous, multi-disciplinary pre-acquisition due diligence protocols to prevent severe capital losses during corporate mergers and market consolidation activities. Thoroughly auditing the historical financial records, local regulatory compliance status, and legacy clinical error rates of target local laboratories prevents the integration of hidden liabilities. Standardizing the laboratory information management software of newly acquired regional clinics within the first ninety days ensures rapid, seamless operational integration into the parent corporate network.

Finally, diagnostic enterprises must proactively establish structured, real-time feedback loops with referring physicians to prevent clinical misalignment and improve testing accuracy. Setting up dedicated medical advisory boards enables diagnostic operators to align their test offerings with the evolving clinical needs of the medical community. This professional collaboration minimizes inappropriate test utilization, enhances clinical interpretation accuracy, and fosters deep, institutional trust between diagnostic centers and primary healthcare providers.

The Carethix Outlook: Key Strategic Takeaways

The imminent transformation of the Indian diagnostics market into a massive USD 124.5 billion powerhouse by 2034 will relentlessly penalize unorganized, low-quality diagnostic operators. Carethix firmly projects that market consolidation will accelerate rapidly, forcing small, unaccredited neighborhood laboratories into financial obsolescence as consumer preferences lean toward standardized services. Corporate executives who delay clinical standardization and fail to secure recognized national quality accreditations will find themselves locked out of profitable corporate insurance contracts and institutional partnerships.

Technological readiness is no longer a luxury but the primary competitive moat that will decisively separate dominant market leaders from struggling legacy players. Investing in advanced molecular diagnostics, integrated digital health ecosystems, and automated laboratory workflows is vital to achieving the operational efficiencies required to sustain enterprise profitability. Enterprise diagnostic chains that fail to aggressively integrate artificial intelligence and digital pathology will continuously struggle with slow turnaround times and high pathologist-related operational costs.

Furthermore, the historic dominance of West India must serve as a clear strategic warning rather than an encouraging blueprint for future nationwide diagnostic expansion. Saturated urban markets in Maharashtra and Gujarat present rapidly diminishing marginal returns, escalating customer acquisition costs, and intense pricing competition among major players. The real growth frontier lies in the underserved tier-2 and tier-3 municipalities where structured hub-and-spoke logistics models can capture vast volumes of untapped clinical diagnostic demand.

Financial discipline must take absolute precedence over aggressive, venture-funded market share acquisition strategies that rely heavily on unsustainable consumer pricing discounts. Uncontrolled price wars initiated by digital aggregators erode industry margins and compromise clinical quality by depriving laboratories of the capital resources needed for continuous modernization. Sustainable profitability belongs exclusively to enterprise operators who focus on high-margin specialty molecular testing, comprehensive corporate wellness programs, and efficient vertical supply chain integration.

Ultimately, the regulatory landscape in India is bound to tighten significantly as state and central government initiatives demand higher clinical accountability and standardized patient data systems. National healthcare programs will increasingly restrict profitable public partnerships to fully accredited laboratory networks, leaving unorganized and unaccredited operators economically isolated from major revenue streams. Proactively aligning clinical and business operational practices with international quality standards is the only viable path to securing long-term institutional survival in this transitioning landscape.

Executive leadership teams must act decisively now by executing targeted strategic investments in technological integration, national quality accreditations, and specialized local clinical talents. The window of opportunity to secure a highly dominant and defensible market position in India’s expanding diagnostic market is narrowing rapidly as institutional capital floods the sector. Those who choose to innovate, standardize, and build robust operational networks today will undoubtedly lead the next generation of global healthcare delivery systems.

FAQs:

Why will India’s diagnostics market reaching USD 124.5 billion by 2034 create a massive healthcare quality crisis instead of just business growth?

India’s diagnostics market may reach USD 124.5 billion by 2034, but nearly 78% of laboratories still operate in the fragmented unorganized sector with inconsistent quality controls and minimal regulatory oversight. This exposes millions of patients to unreliable pathology reports despite diagnostics influencing nearly 70% of all major clinical decisions nationwide. Unless diagnostic chains aggressively standardize NABL accreditation, AI-assisted quality systems, and cold-chain logistics, India risks scaling diagnostic volume faster than diagnostic accuracy.

How does India importing 80%–85% of diagnostic equipment threaten profitability for pathology labs and healthcare investors?

India’s dependency on importing 80% to 85% of medical devices, molecular diagnostic systems, and imaging equipment creates severe exposure to currency volatility, import duties, and global supply-chain disruptions. Many diagnostic operators aggressively cut prices through discount wellness packages while simultaneously facing rising reagent and equipment procurement costs, creating a dangerous long-term margin compression trap. Diagnostic enterprises that fail to localize supply chains and negotiate long-term hedged procurement contracts may struggle to survive the next decade of healthcare consolidation.

Why are tier-2 and tier-3 India becoming the biggest growth opportunity for diagnostic chains despite West India controlling 31.2% market share?

West India captured 31.2% of the diagnostics market in 2025 due to concentrated hospital infrastructure in Maharashtra and Gujarat, but this saturation is rapidly increasing customer acquisition costs and competitive pricing pressure. Meanwhile, underserved tier-2 and tier-3 regions contain enormous untapped preventive healthcare demand with limited access to standardized pathology services. Diagnostic companies that deploy scalable hub-and-spoke laboratory models with digital sample tracking can dominate the next phase of India’s healthcare infrastructure expansion before the market becomes overcrowded.

Why are low-cost digital diagnostic apps and discounted wellness packages creating serious patient safety risks in India?

Many venture-backed digital diagnostic aggregators are aggressively burning capital by offering deeply discounted preventive testing packages without building sufficient accredited laboratory infrastructure. This operational mismatch increases the risk of inaccurate pathology reports, sample contamination, delayed turnaround times, and declining physician trust in digital healthcare ecosystems. Sustainable healthcare growth cannot be built on unsustainable pricing models that sacrifice clinical governance for rapid user acquisition and short-term valuation expansion.

How will NABL accreditation and AI-powered pathology become the biggest competitive advantage in India’s diagnostics industry by 2034?

Less than 3% of India’s estimated 100,000 diagnostic facilities currently possess official NABL accreditation, creating a massive quality credibility gap across the healthcare system. As government regulation tightens and corporate insurance partnerships increasingly favor standardized providers, accredited diagnostic chains with AI-powered pathology workflows will gain disproportionate market trust and institutional revenue access. Healthcare enterprises that delay digital pathology integration, automated workflows, and accreditation expansion risk becoming operationally obsolete in India’s rapidly consolidating diagnostics economy.