GlaxoSmithKline’s $10.6B oncology acquisition strengthens precision cancer care with scalable growth and long-term value creation.

Strategic Case Study: Analyzing GSK’s $10.6 Billion Precision Oncology Bet

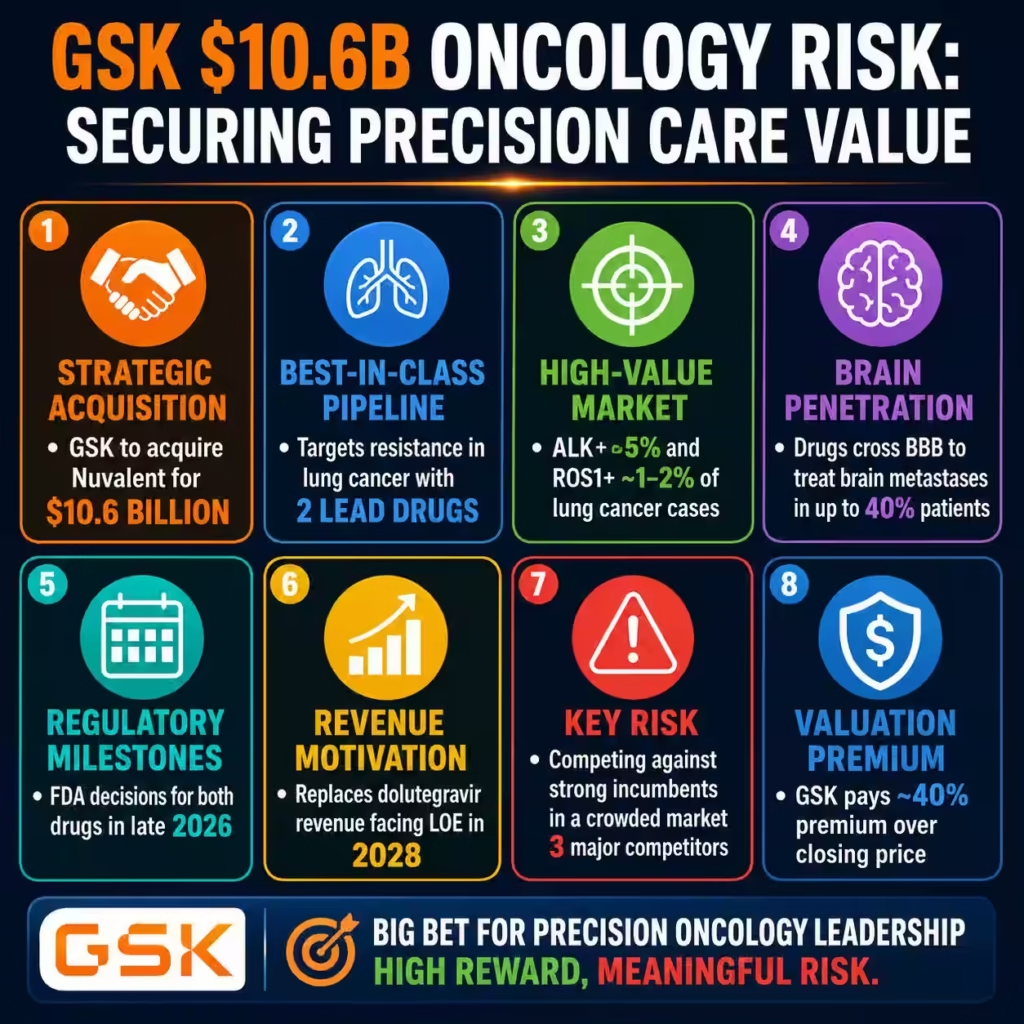

GlaxoSmithKline (GSK) has aggressively re-entered the high-stakes oncology arena by agreeing to acquire Nuvalent for a staggering $10.6 billion in cash, paying $124 per share to secure best-in-class lung cancer assets. This decisive move, announced on June 9, 2026, directly targets the critical clinical failure point of drug resistance in non-small cell lung cancer (NSCLC), a segment valued at billions annually. You can see this acquisition as a textbook maneuver to plug a looming patent cliff revenue gap while addressing the severe unmet need of brain metastases in cancer patients.

The core of this transaction revolves around Nuvalent’s two flagship kinase inhibitors, zidesamtinib (NVL-520) and neladalkib (NVL-655), which are engineered to solve the “resistance trap” that renders current drugs ineffective. Existing therapies often fail when tumors develop specific mutations, such as ROS1 G2032R or ALK G1202R, or when the cancer spreads to the brain where older drugs cannot reach. Nuvalent’s data from the ARROS-1 and ALKOVE-1 trials demonstrated pivotal advancements, showing high objective response rates even in heavily pre-treated patients who had exhausted all other options.

Financially, GSK is paying a 40% premium over Nuvalent’s closing price to lock in these assets before their expected FDA approval decisions in late 2026. The urgency is driven by GSK’s need to replace revenue from its blockbuster HIV drug, dolutegravir, which faces loss of exclusivity starting in 2028. By securing these near-market assets, GSK CEO Luke Miels is betting that the short-term earnings dilution will be vastly outweighed by the long-term revenue streams from these potential multi-blockbuster therapies.

The market for ALK-positive and ROS1-positive NSCLC represents approximately 5% and 1-2% of lung cancer cases respectively, creating a highly defined, lucrative niche for precision medicine. While these percentages seem small, they translate to tens of thousands of patients globally who require chronic, high-cost therapy for years. By controlling the “best-in-class” option that works after other drugs fail, GSK effectively corners the most value-insensitive segment of the market where clinical efficacy dictates prescribing habits.

This acquisition is not merely a purchase of intellectual property but a strategic capture of a proprietary chemical design platform that creates “brain-penetrant” molecules. The Blood-Brain Barrier (BBB) has historically blocked up to 90% of large-molecule drugs, leaving up to 40% of lung cancer patients with untreated brain metastases. Nuvalent’s chemistry allows their drugs to cross this barrier effectively, offering a tangible survival benefit that competitors like Pfizer’s lorlatinib struggle to match without significant toxicity.

Investors reacted swiftly to the news, driving Nuvalent’s stock up by 39%, validating the market’s belief in the quality of the assets and the certainty of the deal closure. GSK’s share price saw a slight dip, a typical reaction to large cash outlays, yet the debt-financed nature of the deal preserves their credit rating. This financial engineering allows GSK to leverage its balance sheet to acquire growth without issuing new equity that would dilute current shareholders.

The regulatory timeline adds a layer of intense pressure and opportunity, with the FDA set to decide on zidesamtinib by September 18, 2026, and neladalkib by November 27, 2026. These dates serve as critical value inflection points where the $10.6 billion investment could either be validated as a bargain or criticized as a gamble. You must recognize that in biotech M&A, paying billions for assets months before approval is a calculated risk to preempt bidding wars.

Ultimately, this case study illustrates the industry-wide pivot from “blockbuster” mass-market drugs to “niche-buster” precision therapies. GSK is acknowledging that the future of oncology lies in genetically defined patient subsets where efficacy is binary: the drug either targets the specific mutation or it doesn’t. By acquiring Nuvalent, GSK transforms its portfolio from a generalist participant to a specialist leader in the precision lung cancer space.

Carethix Critique: Assessing the Risks and Gaps in the $10.6B Valuation

While the strategic logic appears sound on paper, Carethix must critically evaluate whether a $10.6 billion price tag for two late-stage assets in a crowded niche is a prudent allocation of capital. The 40% premium paid by GSK assumes near-perfect execution of the commercial launch and unchallenged clinical superiority, neither of which is guaranteed in the volatile oncology market. You should be skeptical of valuations that price in “best-in-class” status before a drug has generated a single dollar of commercial revenue.

The primary risk lies in the competitive density of the ALK and ROS1 inhibitor markets, which are already populated by entrenched giants like Pfizer, Roche, and Bristol Myers Squibb. Pfizer’s lorlatinib is a formidable third-generation incumbent that has set a high bar for efficacy, meaning Nuvalent’s drugs must show not just non-inferiority, but vastly superior tolerability to justify switching. If the clinical differentiation in real-world settings is marginal rather than transformative, GSK may find itself with an expensive “me-too” product rather than a market leader.

Furthermore, the narrow patient population of ROS1-positive cancers, estimated at fewer than 3,000 new cases annually in the US, raises questions about the return on investment for the zidesamtinib portion of the deal. Even with premium pricing, the total addressable market (TAM) for ROS1 is significantly smaller than for EGFR or KRAS mutations. GSK is essentially banking on the larger ALK market to carry the weight of the $10.6 billion valuation, placing immense pressure on the commercial success of neladalkib.

There is also a significant “execution gap” in GSK’s recent oncology history, specifically with the commercial struggles of previous acquisitions like Tesaro. The company has faced challenges in effectively scaling acquired assets and navigating the complex payer landscape in the United States. Without a radical overhaul of their oncology commercialization infrastructure, GSK risks repeating past mistakes where promising science fails to translate into peak sales performance.

The financial timing of this deal is precarious, as it creates a period of earnings dilution between 2026 and 2028, exactly when the company needs to demonstrate stability to investors. By using debt to finance the deal, GSK increases its leverage ratio in a high-interest-rate environment, potentially constraining its ability to make other necessary strategic moves. You must consider that this “all-in” bet on Nuvalent might hamstring GSK’s ability to diversify into other emerging modalities like antibody-drug conjugates (ADCs) or radioligands.

Clinically, while the “brain-penetrant” claim is compelling, the long-term safety profile of potent CNS-active kinase inhibitors remains a valid concern. Drugs that cross the blood-brain barrier often carry increased risks of neurocognitive side effects, which can severely impact a patient’s quality of life. If post-marketing data reveals unexpected CNS toxicity, the “best-in-class” label could quickly erode, leading to restrictive label warnings and reduced market uptake.

Another critical gap is the reliance on diagnostic testing rates, which are still suboptimal in many community oncology settings globally. For Nuvalent’s drugs to be prescribed, patients must first be tested for the specific ROS1 or ALK mutations, a step that is often missed or delayed. GSK’s success depends not just on selling the drug, but on funding and facilitating the diagnostic infrastructure to find the patients in the first place.

Finally, the acquisition signals a troubling admission that GSK’s internal R&D engine has failed to produce organic growth drivers in oncology. Relying on expensive M&A to fill pipeline holes is a sustainable strategy only if the integration is seamless and the acquired talent is retained. If Nuvalent’s innovative scientists depart post-acquisition, GSK loses the “innovation engine” it paid for, leaving it with just the assets and no platform for future discovery.

Strategic Solutions: Maximizing Value and Patient Impact

To ensure this $10.6 billion investment delivers the projected returns, GSK must implement a multi-faceted commercialization strategy that goes beyond traditional pharmaceutical sales tactics. The first solution is to aggressively position zidesamtinib and neladalkib not just as “later-line” rescue therapies, but as the standard of care for first-line treatment in patients with brain metastases. By generating head-to-head data against current standards like crizotinib and alectinib, GSK can move their assets up the treatment paradigm where patient duration is longer and revenue potential is higher.

GSK should leverage its global footprint to accelerate the approval and reimbursement of these drugs in key ex-US markets like China and Japan, where lung cancer incidence is significantly higher. The Asian market has a higher prevalence of EGFR and ALK mutations compared to Western populations, presenting a massive, under-served volume opportunity. You can capture significant value by tailoring pricing and access programs specifically for these high-volume regions to drive rapid volume uptake upon approval.

Financially, GSK needs to employ innovative “value-based contracting” models with US payers to overcome the resistance to high oncology drug prices. By offering rebates or refunds for patients who do not achieve a specific duration of response, GSK can de-risk the adoption of their high-cost therapies for insurers. This confidence-based pricing strategy effectively communicates faith in the “best-in-class” durability of their products and can secure preferred formulary status over competitors.

To solve the diagnostic gap, GSK must invest heavily in Next-Generation Sequencing (NGS) partnerships with major diagnostic firms like Foundation Medicine and Guardant Health. Sponsoring “reflex testing” programs where pathologists automatically test for ALK and ROS1 mutations upon a lung cancer diagnosis can significantly expand the identified patient pool. You ensure that every eligible patient is identified immediately, thereby maximizing the “capture rate” for the new therapies.

Operational integration must focus on preserving the agile, scientific culture of Nuvalent while plugging it into GSK’s massive clinical operations machine. GSK should establish a “center of excellence” for precision oncology in Cambridge, Massachusetts, allowing the Nuvalent team to operate with a degree of autonomy. This “reverse integration”—where the acquirer adapts to the target’s culture—is often the solution to the talent flight that plagues biotech acquisitions.

Another critical solution is to explore combination therapies immediately, pairing these kinase inhibitors with chemotherapy or immunotherapy to prevent the emergence of new resistance mutations. By attacking the tumor from multiple biological angles, GSK can potentially extend the “progression-free survival” (PFS) well beyond the current industry benchmarks. You can create a “moat” around these assets by proving that they work best as the backbone of a combination regimen, making them indispensable.

Digital health solutions should be deployed to monitor patient side effects in real-time, specifically to manage the unique toxicity profiles of CNS-active drugs. Developing a companion app that tracks neurocognitive symptoms can help physicians dose-adjust proactively, keeping patients on therapy longer. This focus on “total patient experience” differentiates a high-priced drug from a commodity generic and justifies the premium to prescribers.

Finally, GSK needs to utilize the “halo effect” of these advanced therapies to revitalize its entire oncology brand image. Marketing these successes aggressively to the scientific community helps recruit top talent and rebuild relationships with key opinion leaders (KOLs) who may have been skeptical of GSK’s commitment to cancer. You transform the corporate narrative from “rebuilding” to “leading” by showcasing these assets as proof of a new, scientifically rigorous era at GSK.

Prevention Methods: Safeguarding Against Future Pipeline and Clinical Failures

Preventing the recurrence of the “pipeline gap” that necessitated this $10.6 billion outlay requires a fundamental shift in GSK’s internal Research & Development strategy. The most effective prevention step is the implementation of a continuous, small-cap business development program rather than relying on desperate, massive acquisitions. By making smaller, earlier-stage bets in the $500 million to $1 billion range, you distribute risk across a broader portfolio and avoid the “winner-take-all” pressure of a mega-deal.

To prevent clinical failure due to drug resistance, the industry must adopt adaptive clinical trial designs that anticipate tumor evolution before it happens. Instead of waiting for a drug to fail, future trials should include “liquid biopsy” monitoring at regular intervals to detect rising resistance clones in the blood. This allows for “switch maintenance” strategies where therapy is modified in real-time based on the genetic drift of the tumor, preventing clinical relapse.

Companies must also prevent the “siloing” of scientific data by integrating Artificial Intelligence (AI) into their drug discovery platforms to predict resistance mutations years in advance. By simulating how a kinase inhibitor interacts with a protein structure using AI, researchers can design “future-proof” molecules that account for likely mutations before they even appear in patients. You can save billions in failed trials by virtually stress-testing molecules against thousands of potential resistance profiles before a single patient is dosed.

Financial prevention involves strict capital allocation discipline, ensuring that R&D budgets are protected even during periods of revenue pressure. GSK must ring-fence its early discovery budget to prevent the “starvation” of internal innovation that often occurs when commercial products lose patent protection. You ensure a steady stream of homegrown INDs (Investigational New Drug applications) by treating R&D as a fixed, non-negotiable operating cost rather than a discretionary expense.

To prevent market access barriers, pharmaceutical companies must engage with payers and health technology assessment (HTA) bodies two to three years before launch. Early dialogue regarding the “evidence requirements” for reimbursement prevents the scenario where a drug is approved but not covered. You must co-create the value dossier with payers to ensure that the clinical trial endpoints match what insurers are willing to pay for.

Talent retention strategies are critical to prevent the “brain drain” that erodes a company’s scientific IQ over time. Implementing “intrapreneurship” programs where internal scientists are given funding and autonomy to pursue high-risk projects can mimic the biotech startup environment within a pharma giant. You keep your best innovators engaged by giving them the freedom to fail and the resources to succeed without bureaucratic suffocation.

Finally, preventing “strategic drift” requires a stable, long-term leadership vision that does not oscillate with every CEO change. The board of directors must mandate a 10-year oncology roadmap that survives executive turnover, ensuring consistency in therapeutic focus. You build a resilient organization by anchoring strategy in scientific fundamentals rather than the quarterly earnings cycle or the whims of new management.

Key Takeaway

Carethix’s Verdict: GSK’s $10.6 billion acquisition of Nuvalent is a necessary, albeit expensive, surgical strike to save its oncology future. While the 40% premium is steep, the cost of irrelevance in the precision oncology market is far higher. The deal successfully secures a lifeline for the post-2028 patent cliff, but it shifts the burden of proof entirely to commercial execution. The science of zidesamtinib and neladalkib is robust; now, Luke Miels must prove that GSK can sell high-science innovation as effectively as it buys it. For you, the stakeholder, this is a signal to watch for aggressive clinical differentiation and rapid Asian market expansion as the true indicators of value creation. Victory will belong to the swift, not just the rich.