Breast cancer’s 12.9% risk crisis urges organizations to optimize health strategy and protect healthcare margins.

Analyzing the Illusion of Behavioral Immunity in Enterprise Healthcare

Sudden breast cancer diagnoses in health-conscious individuals expose a flaw in corporate wellness programs that equate healthy habits with clinical immunity. This reality reveals systemic benefit gaps that leave self-insured funds vulnerable to oncological claims. By examining the lifestyle and biology gap, sponsors can better manage the financial risks of cancer.

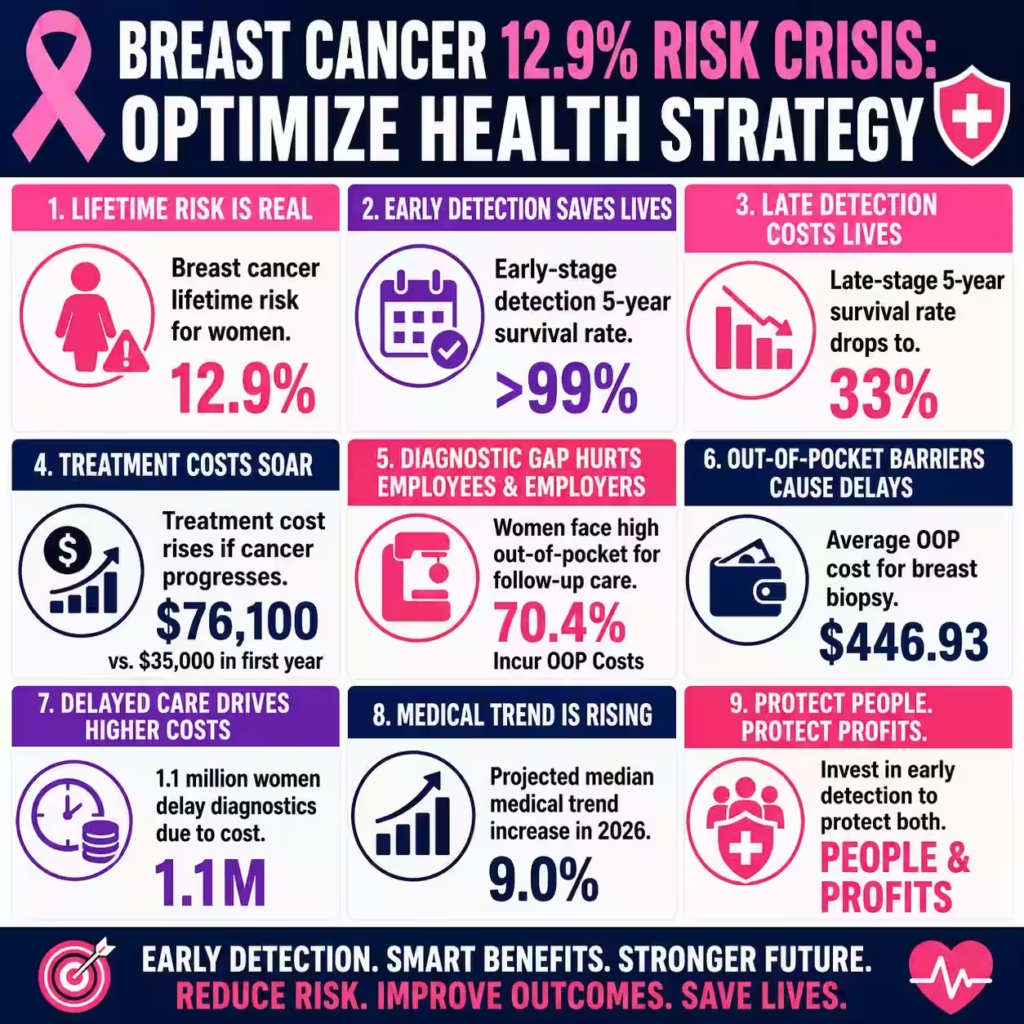

National oncology data from the United States indicates that approximately 279,731 new cases of invasive breast cancer are diagnosed annually among women, representing a persistent 12.9% lifetime risk. While healthy behavior mitigates cardiovascular and metabolic liabilities, it cannot neutralize underlying genetic mutations such as BRCA1 and BRCA2, which substantially increase individual disease susceptibility. Consequently, self-insured employers face a continuous financial exposure if their health programs rely strictly on voluntary behavioral modifications rather than structured, high-resolution diagnostic screening.

Actuarial data shows breast cancer treatment costs commercial plans $35,000 in the first year, escalating to $76,100 if progression occurs due to delayed follow-up. Consequently, early detection is a critical capital conservation strategy for risk managers.

Despite monthly self-exams, detecting non-palpable calcifications requires advanced technologies like digital tomosynthesis or MRI. Current benefit barriers to these diagnostics cause delays, forcing employers to absorb higher medical claims and absenteeism costs.

Statistical models from the Centers for Disease Control and Prevention confirm that early-stage localized detection yields a five-year survival rate exceeding 99%. In sharp contrast, late-stage metastatic diagnoses cause a five-year survival rate of only 33%, demonstrating the impact of delayed clinical intervention. By removing the financial friction points that deter rapid diagnostic confirmation, corporate health sponsors can actively shift their employee demographic toward early-stage, curable clinical pathways.

This business analysis shows that the historic boundary between basic preventive wellness and active oncology intervention must be permanently dissolved. Enterprise leadership must recognize that a healthy workforce is not a guaranteed shield against high-cost clinical claims. Strategic benefit redesign represents a reliable methodology to stabilize corporate healthcare spending while preserving valuable human capital.

Consequently, health benefits consultants must guide self-insured employers toward data-driven, evidence-based coverage solutions. Aligning corporate financial interests with proactive clinical methodologies ensures that claims risk is managed with precision. This analytical paradigm represents the future of corporate health stewardship in a highly volatile healthcare economic landscape.

The Carethix Critique: Systemic Risks and Gaps in Traditional Employer Coverage

Conventional corporate health benefit architectures possess a fundamental structural deficiency by bifurcating complimentary preventive screenings from high-cost subsequent diagnostic interventions. Although the Affordable Care Act stipulates zero out-of-pocket expenditures for standardized screening mammography, subsequent diagnostic examinations frequently necessitate substantial cost-sharing from employees. Carethix contends that this systemic fragmentation establishes a significant obstacle for personnel who encounter abnormal screening findings, thereby discouraging the timely pursuit of clinical resolution.

Empirical market data indicates that in 2023, 70.4% of patients with commercial insurance coverage incurred considerable out-of-pocket liabilities for essential follow-up diagnostic assessments. These unforeseen clinical costs yielded an overall average of $169.27, while specialized interventions, such as breast biopsies, reached an average out-of-pocket expenditure of $446.93. This financial burden inhibits more than 1.1 million women from obtaining expedited diagnostic evaluations, a phenomenon that directly contributes to the diagnosis of advanced clinical stages.

Employers are currently exposing their organizations to severe financial risks by accepting these high diagnostic cost-sharing models within their third-party administrator contracts. When an employee delays a diagnostic biopsy due to out-of-pocket cost concerns, the underlying tumor continues to replicate without therapeutic intervention. This delay frequently results in stage migration, which transforms a highly treatable localized condition into a complex, late-stage oncological case.

The 2026 Employer Health Care Strategy Survey predicts a 9.0% median medical benefit trend increase for self-insured firms. This escalation is primarily driven by late-stage oncology treatment costs, which can reach hundreds of thousands of dollars per patient. Carethix asserts that maintaining standard high-deductible health plans without diagnostic carve-outs is a major strategic failure that undermines corporate fiscal health.

The indirect costs of this systemic diagnostic gap are equally severe, manifest in extensive productivity losses, elevated short-term disability claims, and permanent talent attrition. When an employee must undergo aggressive, systemic chemotherapy for an advanced tumor, the business suffers from prolonged absenteeism and reduced operational efficiency. These unquantified indirect expenses often exceed the direct medical costs of early-stage, localized surgical interventions.

Traditional wellness initiatives and employee assistance programs are fundamentally unequipped to manage the intricate psychological toll associated with oncology navigation. Employees are left to navigate a fragmented healthcare system while managing financial anxiety and complex treatment decisions. Corporate sponsors must bridge these operational gaps by establishing integrated, friction-free diagnostic pathways that protect their workforce from clinical and financial toxicity.

Furthermore, standard wellness metrics focus excessively on superficial engagement rather than measurable clinical risk reduction. This disproportionate emphasis results in a suboptimal perception of security among corporate executives, who consequently disregard the escalating latent oncological liabilities within their respective employee populations. Carethix characterizes this diagnostic-to-treatment disparity as the most significant unmitigated risk factor currently present in employer-sponsored healthcare frameworks.

Strategic Business and Operational Solutions for Commercial Health Sponsors

To mitigate clinical and financial risks, self-insured employers should adopt value-based designs that eliminate diagnostic cost-sharing. By covering follow-up mammograms, ultrasounds, and biopsies at 100%, sponsors remove barriers to timely care. Actuarial modeling indicates that absorbing the modest $169 average cost of diagnostic testing prevents late-stage oncological claims that average over $127,000 per patient.

Enterprises should establish direct contracting agreements with oncology Centers of Excellence that utilize advanced digital breast tomosynthesis. These high-performing clinical networks leverage specialized diagnostic radiologists who achieve higher accuracy rates than general imaging centers.

By leveraging specialized Centers of Excellence, plan sponsors can achieve a 1.5% to 2.0% reduction in redundant patient recall rates. This strategic alignment significantly curtails both diagnostic and administrative overhead.

Furthermore, the implementation of employer-sponsored pharmacogenomic and hereditary genetic screening programs constitutes a highly effective financial strategy for risk mitigation. Providing covered employees with voluntary access to clinical-grade BRCA1 and BRCA2 testing allows for the early identification of high-risk cohorts. This predictive insight enables benefits managers to authorize customized, risk-adjusted surveillance protocols, such as annual diagnostic magnetic resonance imaging, long before standard age thresholds.

Corporate health sponsors must also renegotiate their contracts with Pharmacy Benefit Managers to curb the escalating cost of specialty oncology drugs. In 2024, specialty pharmaceutical spend consumed nearly 24% of the total employer healthcare dollar, with oncology therapeutics representing a primary driver of this expenditure. Implementing mandatory biosimilar substitution protocols and prior authorization criteria ensures clinical efficacy while maintaining benefit plan solvency.

The implementation of specialized clinical care navigation platforms provides a robust operational framework for guiding diagnosed personnel through the intricacies of the oncology landscape. Certified nurse navigators facilitate expedited follow-up consultations, synchronize multidisciplinary medical teams, and provide access to relevant clinical trials. This bespoke advocacy serves to mitigate clinical latency, alleviate psychological distress for the employee, and optimize the timeline for professional reintegration.

Ultimately, self-insured corporations have the unique financial flexibility to redesign their medical benefits to align with modern precision medicine. Investing in proactive diagnostic coverage shields the enterprise’s balance sheet from high-cost, multi-stage oncology claims. These strategic enhancements position the organization as an employer of choice while ensuring long-term healthcare cost predictability.

These integrated financial strategies enable self-insured employers to stabilize their yearly premium increases while providing high-value care. Implementing clinical navigation and value-based benefits creates a sustainable, resilient ecosystem that serves both employer and employee. Transitioning to these strategic solutions converts healthcare management from an unpredictable cost liability into a managed organizational asset.

Proactive Prevention Strategies and Future-Proofing Employee Wellness

Future-proofing corporate healthcare requires shifting from reactive oncology to proactive cellular health optimization. Enterprises must launch workplace campaigns educating employees on monthly breast self-examinations to detect early physical changes. Instructing employees on how to spend ten minutes once a month checking for anomalies can lead to early detection of physical changes before clinical symptoms worsen.

Employers must expand specialized women’s health benefits to target key risk factors across all career stages and age groups. Industry data from 2026 shows that 58% of progressive corporate sponsors are actively expanding their women’s health offerings, representing a substantial increase from previous benefit cycles. Deploying comprehensive frameworks for endocrine wellness and perimenopausal clinical oversight enables enterprises to mitigate the systemic biological irregularities often linked to heightened oncological liabilities.

Workplace wellness programs should be redesigned to integrate advanced epigenetic and environmental risk assessments alongside standard biometric screenings. Self-insured companies can audit their physical facilities to eliminate exposure to known endocrine-disrupting chemicals and industrial carcinogens. Proactively reducing environmental toxins promotes cellular health and lowers non-hereditary cancer rates.

Commercial health sponsors should utilize high-resolution predictive analytics to expose latent screening non-compliance across diverse demographic and geographic employee sectors. Through the rigorous analysis of anonymized longitudinal claims data, plan administrators can isolate specific operational units or regional territories exhibiting suboptimal mammography utilization metrics. This analytical precision facilitates the deployment of specialized, risk-adjusted communication strategies designed to drive clinical adherence within these vulnerable cohorts.

Furthermore, corporate nutritional and fitness benefits must pivot away from generic weight loss goals toward optimizing systemic physiological resilience. Structured programs that promote high-intensity physical activity and anti-inflammatory dietary patterns help regulate circulating estrogen levels and improve insulin sensitivity. While a healthy lifestyle cannot guarantee immunity from genetic mutations, maximizing metabolic health significantly enhances the body’s natural defense mechanisms.

Finally, corporate benefits leaders must partner with clinical advisory boards to continually update coverage parameters as new technologies emerge. As multi-cancer early detection liquid biopsies and advanced biomarker tests gain regulatory approval, medical plans must rapidly incorporate these diagnostic innovations. Staying ahead of the clinical innovation curve allows enterprises to intercept oncological risks early, protecting both their employees and their financial reserves.

In conclusion, organizations that foster a culture centered on extensive preventative health are more resilient against the escalating financial burdens of chronic disease. By providing workers with the advanced clinical tools and education needed to manage their health, companies create an active line of defense. Proactive prevention remains the most effective hedge against the unpredictable nature of biological risks in the modern workplace.

Carethix’s Key Takeaway: The Imperative for Decisive Corporate Leadership

The empirical emergence of breast cancer within health-conscious demographics demonstrates that passive wellness architectures are fundamentally insufficient for robust institutional risk management. Enterprise executives must move beyond superficial digital engagement platforms that delegate substantial diagnostic liabilities to their personnel. Maintaining legacy high-deductible benefit frameworks constitutes a significant strategic oversight and a direct threat to long-term corporate fiscal stability.

True executive leadership demands that self-insured enterprises view healthcare benefits as a high-leverage capital investment rather than a mere cost center. Eliminating out-of-pocket barriers for follow-up diagnostic procedures is the single most effective action a health sponsor can take today. This decisive intervention protects valuable employees from financial toxicity while safeguarding the enterprise from uncontrolled specialty pharmacy claims.

Human capital is the most critical asset of any modern organization, and its physical preservation must be prioritized above short-term margin optimizations. When an employer provides comprehensive, friction-free diagnostic coverage, it establishes a culture of psychological safety and organizational trust. Employees who feel genuinely protected by their organization are significantly more likely to remain loyal, highly engaged, and productive.

The projected 9.0% medical trend increase for 2026 serves as an urgent wake-up call for benefits officers across the country. Only those organizations that aggressively reform their medical benefit architectures will survive this coming period of intense healthcare inflation. Carethix strongly advises executive boards to implement these diagnostic coverage reforms before escalating oncology claims compromise overall business profitability.

Behavioral wellness is not a guaranteed shield against genetic biology, but modern diagnostic early detection is a highly reliable safeguard for human life. The strategic choice facing corporate leadership is clear: invest in modest diagnostic coverage today, or face escalating treatment costs tomorrow. We urge you to take immediate action to align your benefits structure with the realities of modern clinical science.

Failing to act now will leave your enterprise vulnerable to the rising tide of high-cost oncology claims and employee dissatisfaction. By implementing these recommended diagnostic solutions, you can lead your industry in both clinical excellence and fiscal stewardship. The data has spoken, the path forward is defined, and the responsibility to execute this strategic evolution rests entirely with you.

Your organization has the power to redefine the standard of employee care while securing a sustainable competitive advantage. Do not wait for the next major oncology claim to expose the systematic weaknesses in your current plan design. Partner with Carethix today to deploy a resilient, clinical-grade benefits strategy that protects your people and your profits.

FAQs:

1. Why do healthy women still face a 12.9% lifetime breast cancer risk despite exercise and healthy lifestyles?

A 12.9% lifetime breast cancer risk exposes the dangerous assumption that healthy habits create clinical immunity when genetics, hormonal factors, and biological variability remain powerful risk drivers. Relying solely on wellness programs while ignoring diagnostic access creates a false sense of security that increases financial and clinical exposure. Organizations promoting prevention without investing in early detection infrastructure are underestimating the true economics of oncology risk.

2. How much does delayed breast cancer diagnosis cost employers and self-insured health plans?

The financial impact is substantial because first-year treatment averages roughly $35,000 but can escalate beyond $76,100 when delayed diagnosis drives disease progression. Employers focused only on premium management while maintaining diagnostic barriers may unintentionally create significantly larger downstream claims exposure. Small upfront investments in follow-up diagnostics often cost far less than absorbing advanced oncology expenses and productivity losses.

3. Why are breast cancer diagnostic costs causing over 1.1 million women to delay follow-up care?

When 70.4% of commercially insured patients face out-of-pocket costs averaging $169.27 for initial follow-up assessments—with specialized interventions like breast biopsies climbing to an average of $446.93—financial friction becomes a major healthcare failure point. High deductibles shift clinical decision-making from physicians to personal finances, increasing the probability of delayed treatment pathways. Organizations accepting these barriers are effectively transferring short-term savings into long-term, high-cost risk accumulation.

4. Does early breast cancer detection really improve survival rates and reduce healthcare spending?

The difference is dramatic because localized detection produces survival rates exceeding 99%, while metastatic disease reduces five-year survival to roughly 33%. Delayed diagnostics create both human costs and financial inefficiencies because advanced-stage treatment requires significantly more expensive therapies, longer absences, and higher specialty drug utilization. Companies prioritizing rapid diagnostic access are often protecting both workforce stability and balance sheet performance.

5. Why are self-insured employers facing a projected 9.0% healthcare cost increase from oncology trends?

Projected medical trend increases near 9.0% highlight how traditional wellness programs alone are failing to address expensive oncology risk accumulation. Rising specialty drug utilization, delayed diagnoses, absenteeism, and advanced-stage treatment expenses collectively create sustained pressure on employer-sponsored plans. Organizations that continue treating diagnostic access as a cost center rather than a risk management tool may face increasing volatility in future healthcare spending.